- Abuse & The Abuser

- Achievement

- Activity, Fitness & Sport

- Aging & Maturity

- Altruism & Kindness

- Atrocities, Racism & Inequality

- Challenges & Pitfalls

- Choices & Decisions

- Communication Skills

- Crime & Punishment

- Dangerous Situations

- Dealing with Addictions

- Debatable Issues & Moral Questions

- Determination & Achievement

- Diet & Nutrition

- Employment & Career

- Ethical dilemmas

- Experience & Adventure

- Faith, Something to Believe in

- Fears & Phobias

- Friends & Acquaintances

- Habits. Good & Bad

- Honour & Respect

- Human Nature

- Image & Uniqueness

- Immediate Family Relations

- Influence & Negotiation

- Interdependence & Independence

- Life's Big Questions

- Love, Dating & Marriage

- Manners & Etiquette

- Money & Finances

- Moods & Emotions

- Other Beneficial Approaches

- Other Relationships

- Overall health

- Passions & Strengths

- Peace & Forgiveness

- Personal Change

- Personal Development

- Politics & Governance

- Positive & Negative Attitudes

- Rights & Freedom

- Self Harm & Self Sabotage

- Sexual Preferences

- Sexual Relations

- Sins

- Thanks & Gratitude

- The Legacy We Leave

- The Search for Happiness

- Time. Past, present & Future

- Today's World, Projecting Tomorrow

- Truth & Character

- Unattractive Qualities

- Wisdom & Knowledge

FOLLOWERS

0

Users

Career & Finance Fridays

Zero Based Budgeting

Do you know where all your money goes each month? If you’re like many people, the answer might be a vague "somewhere." This is where zero-based budgeting comes in, and it’s a method that has truly transformed how I think about my finances.

The basic idea of zero-based budgeting is simple: every dollar you earn is assigned a job. Before the month even begins, you allocate your entire income to expenses, savings, and debt repayment, until your income minus your expenses equals zero. The goal is to give every single dollar a purpose and a job.

For years, I operated on a more traditional budget where I would track my spending after the fact. I kept “guidelines” around different categories, but didn’t hold firmly to those numbers. For example, if diapers were on sale, I would stock up and blow my “kid expenses” category out of the water. While this method of budgeting helped me have better control of my money, I often found myself wondering why I was short on funds at the end of the month or where certain chunks of money had disappeared to. Implementing a zero-based budget felt intimidating at first, requiring a detailed look at every single outflow. But the clarity it brought was incredible. It meant that I had to plan for those extra diapers, or move money from one category to another so that I didn’t overspend.

When you sit down and actively decide where each dollar goes, you gain immense control. You might realize you’re spending too much on eating out, or that you have extra money to put towards a specific savings goal. It forces you to be intentional and proactive with your money, rather than reactive.

It's a misconception that zero-based budgeting is restrictive. In reality, it’s quite freeing. You’re not just mindlessly spending; you’re making conscious decisions that align with your financial goals. If you want to save for a vacation, you allocate money to that line item. If you have unexpected expenses, you adjust other categories to accommodate them.

If you’ve been struggling to get a handle on your finances, or if you simply want more clarity and control, I highly recommend giving zero-based budgeting a try. It might take a little effort to set up initially, but the peace of mind and financial insight it provides are invaluable. Trust me, it’s going to take a few months to get things dialed in, but it will be worth it!

Interesting Fact #1

The zero-based budgeting method, also known as the ZBB budget, encourages you to use every penny of your monthly income. But that doesn’t mean spending it on a shopping spree. Important goals, such as saving money and paying off debt — as well as spending on fun stuff — are all part of the plan.

Interesting Fact #2

The idea behind the zero-based budget, sometimes also called the zero-sum budget, is to give every cent a purpose.

Interesting Fact #3

Zero-based budgeting is a method that has you allocate all of your money to expenses for needs and wants, as well as short- and long-term savings and debt payments. The goal is that your income minus your expenditures equals zero by the end of the month.

Quote of the day

“Most people aren’t broke because of income—they’re broke because of ignorance.” ― Joseph C. Kunz Jr.

Article of the day - Master Zero-Based Budgeting: A Comprehensive Guide

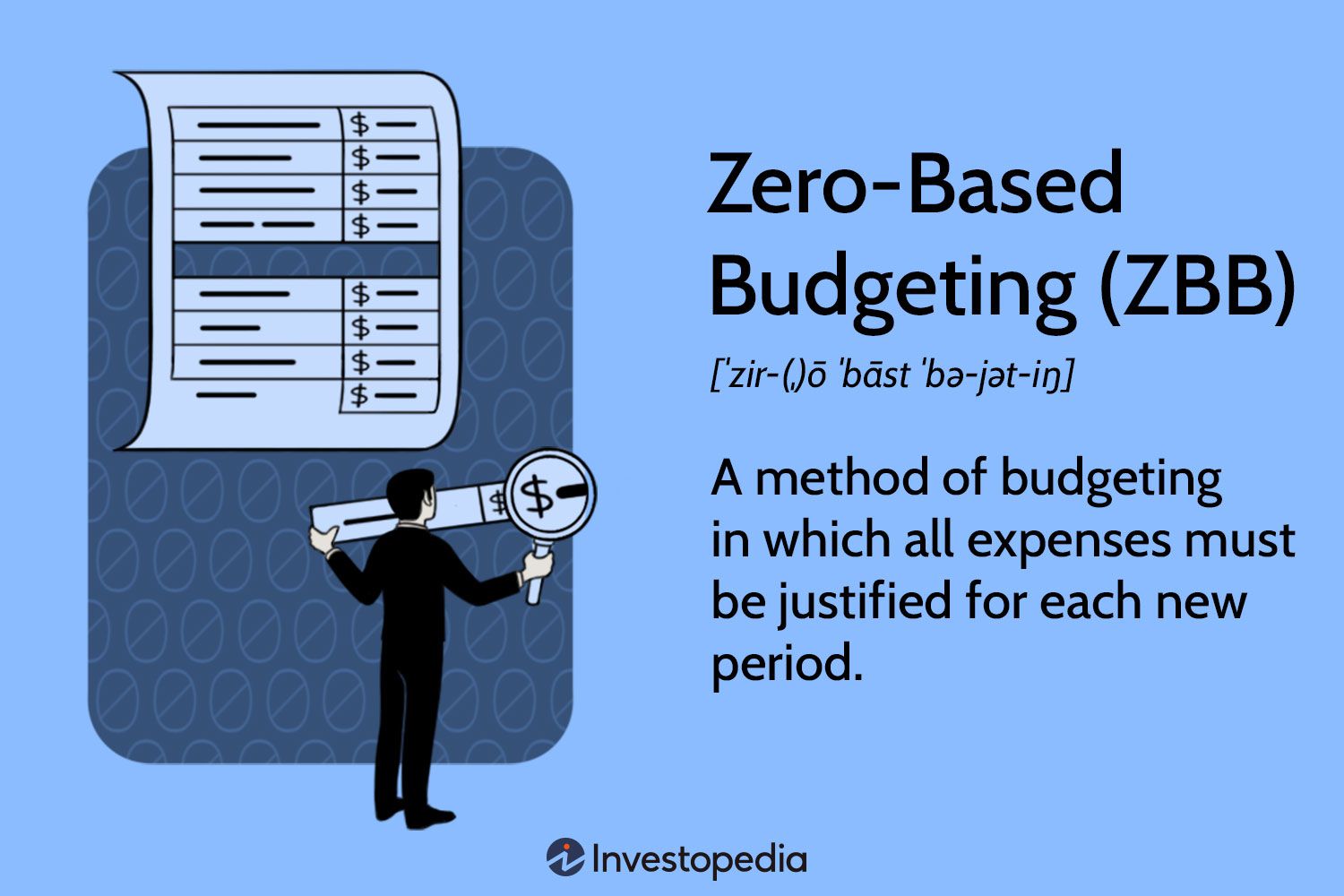

What Is Zero-Based Budgeting (ZBB)?

Zero-based budgeting (ZBB) is an intensive budgeting technique that requires justifying all expenses from a 'zero base' for each new period. Unlike traditional budgeting, which generally increases on prior budgets, ZBB involves analyzing and justifying each cost, focusing on strategic objectives and financial efficiency. Though primarily utilized by companies to identify and cut unnecessary expenditures, individuals and families can also adopt ZBB to improve their financial decision-making.

Key Takeaways

- Zero-based budgeting requires every expense to be justified for each period, starting from a "zero base."

- This budgeting method can lower costs by avoiding automatic increases based on prior budgets.

- Zero-based budgeting is time-consuming but offers detailed insights compared to traditional incremental budgeting.

- It tends to favor operations that generate direct revenue, potentially underfunding long-term projects like R&D.

- While mainly used by businesses, zero-based budgeting can also be beneficial for individuals and families.

:max_bytes(150000):strip_icc():format(webp)/Term-Definitions_Zero-based-budgeting-101715d3484b488581579d0a729a6d47.jpg)

Mira Norian / Investopedia

Implementing Zero-Based Budgeting in Organizations

Zero-based budgeting helps align top-level goals with specific areas of an organization during the budgeting process. Costs are grouped and compared to past results and current expectations.

Zero-based budgeting can be ongoing for years, with only a few functional areas reviewed at a time due to its detailed nature. It can help reduce costs by preventing blanket budget changes, though it is more time-consuming than traditional budgeting.1

Important

This practice favors areas with direct revenues or production, as their contributions are easier to justify than those in departments like client service and research and development.

While primarily used in business, individuals and families can also adopt zero-based budgeting.

Comparing Zero-Based Budgeting to Traditional Budgeting

Traditional budgeting typically involves incremental increases, like a 2% rise in spending over previous budgets. Zero-based budgeting requires a justification of both old and new expenses.

Traditional budgeting also only analyzes new expenditures. ZBB starts from zero and calls for a justification of old, recurring expenses in addition to new expenditures. Zero-based budgeting aims to put the onus on managers to justify expenses. It drives value for an organization by optimizing costs, not just revenue.

Real-World Example of Zero-Based Budgeting

Imagine a construction equipment company using zero-based budgeting to closely examine its manufacturing expenses. The company sees that the cost of some outsourced parts rises by 5% annually.

The company can make those parts in-house with its workers. It finds that, after weighing the positives and negatives of in-house manufacturing, it can make the parts cheaper than the outside supplier.

The company can identify a situation in which it can decide to make the part itself or buy the part from an external supplier for its end products instead of blindly increasing the budget by a certain percentage and masking the cost increase.

Traditional budgeting may not allow cost drivers within departments to be identified, but zero-based budgeting is a more granular process that aims to identify and justify expenditures. Zero-based budgeting is also more involved, however, so the costs of the process itself must be weighed against the savings it might identify.

What Is Zero-Based Budgeting?

Zero-based budgeting was created in the late 1960s by former Texas Instruments account manager Peter Pyhrr.2

Zero-based budgeting starts at zero, unlike traditional budgeting. It justifies each expense for a reporting period.

Zero-based budgeting starts from scratch, analyzing each granular need of the company instead of using the incremental budgeting increases found in traditional budgeting. This essentially allows for a strategic, top-down approach to analyze the performance of a given project.

What Are the Advantages of Zero-Based Budgeting?

Zero-based budgeting offers several advantages, including focused operations, lower costs, budget flexibility, and strategic execution. The highest revenue-generating operations come into greater focus when managers think about how each dollar is spent. Zero-based budgeting can reduce costs by preventing resource misallocation seen in incremental budgeting.

What Are the Disadvantages of Zero-Based Budgeting?

Zero-based budgeting has several disadvantages. It's time- and resource-intensive. The time cost may not be worth it since a new budget is created each period. Using a modified budget template instead may prove more beneficial.3

ZBB might favor short-term perspectives by giving more resources to operations with the highest revenues. As a result, areas like research and development or long-term projects may be overlooked.

The Bottom Line

Zero-based budgeting (ZBB) offers a detailed approach to financial planning by requiring justification for all expenses each period. Unlike traditional budgeting, which increments past budgets, ZBB starts from scratch, ensuring that every financial decision aligns with current organizational goals. This method promotes cost efficiency by preventing the automatic growth of budgets and encourages strategic spending. Although time-intensive, its focus on optimizing costs can lead to significant long-term savings and strategic financial management for both companies and individuals.

Question of the day - Have you ever tried zero-based budgeting, or do you have another budgeting method that works well for you?

Money & Finances

Have you ever tried zero-based budgeting, or do you have another budgeting method that works well for you?

Daily archives

Current Survey

Top 5 Contributors (Oct)

20209 pts

12060 pts

10714 pts

10417 pts

10117 pts