- Abuse & The Abuser

- Achievement

- Activity, Fitness & Sport

- Aging & Maturity

- Altruism & Kindness

- Atrocities, Racism & Inequality

- Challenges & Pitfalls

- Choices & Decisions

- Communication Skills

- Crime & Punishment

- Dangerous Situations

- Dealing with Addictions

- Debatable Issues & Moral Questions

- Determination & Achievement

- Diet & Nutrition

- Employment & Career

- Ethical dilemmas

- Experience & Adventure

- Faith, Something to Believe in

- Fears & Phobias

- Friends & Acquaintances

- Habits. Good & Bad

- Honour & Respect

- Human Nature

- Image & Uniqueness

- Immediate Family Relations

- Influence & Negotiation

- Interdependence & Independence

- Life's Big Questions

- Love, Dating & Marriage

- Manners & Etiquette

- Money & Finances

- Moods & Emotions

- Other Beneficial Approaches

- Other Relationships

- Overall health

- Passions & Strengths

- Peace & Forgiveness

- Personal Change

- Personal Development

- Politics & Governance

- Positive & Negative Attitudes

- Rights & Freedom

- Self Harm & Self Sabotage

- Sexual Preferences

- Sexual Relations

- Sins

- Thanks & Gratitude

- The Legacy We Leave

- The Search for Happiness

- Time. Past, present & Future

- Today's World, Projecting Tomorrow

- Truth & Character

- Unattractive Qualities

- Wisdom & Knowledge

FOLLOWERS

0

Users

Career & Finance Fridays

Ways to Improve Your Finances

Financial growth - both in dollar amount and personal - is an important part of life. Your financial health has a big impact on your future, potential, and quality of life - so improving it is a great way to build into your future. It can be easy to feel as though improving your finances is simply done through making more money, but that's not necessarily true.

You can improve your finances in a number of ways, many of which simply take a little bit of strategic planning.

1. Reevaluate your lifestyle

Go over your spending. What areas of life are you thriving in, and what ones could take a little editing? Where do you find yourself getting caught up spending more than you'd like to? Are there things you can cut out? Giving your lifestyle a simple once-over every now and then can help you identify any problematic or unnecessary areas.

2. Improve your credit score

Your credit score may or may not seem like a big deal right now - but in the long run, it's really, really important. Your credit score affects your ability to get loans for things like cars, houses, and other big purchases. Investing in this part of your financial portfolio will affect your long-term future in some huge ways.

3. Make a budget

It's simple, but effective. Create a monthly budget for your spending, and stick to it. Find a routine that seems sustainable, and look for ways that you can actually, practically, be consistent.

Your financial health isn't about bragging rights or riches. It's about security and stability - things that support and stabilize your future. Invest in yourself. In the life you're trying to create.

Interesting Fact #1

Lack of financial literacy cost Americans $450 billion in 2020.

Interesting Fact #2

63% of people had their personal finances affected by Covid.

Interesting Fact #3

Only 30% of Americans have a long-term financial plan.

Quote of the day

Money is a terrible master but an excellent servant.

- P. T. Barnum

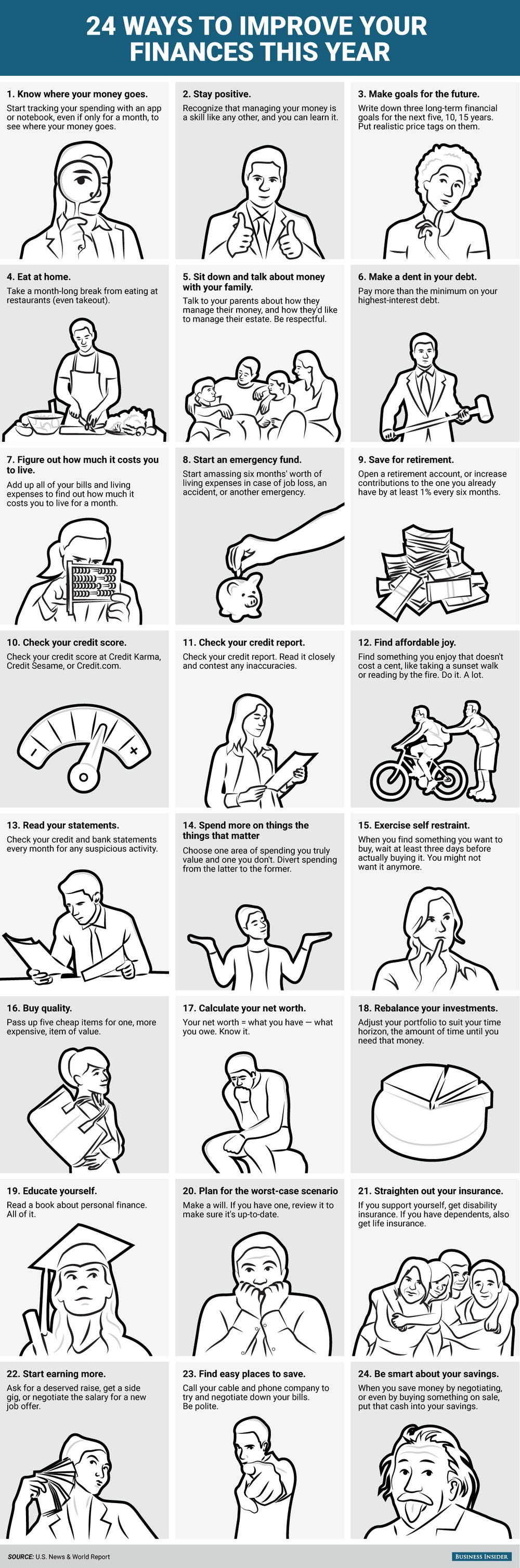

Article of the day - 15 Ways to Improve Your Finances

You are reading the right article if you have intentions of improving your finances. It is true that the state of your finances affects every other aspect of your life.

In order to improve other aspects of your life, learning to improve your finances is necessary. Surprisingly, getting a hang of this crucial part of one’s life is simple. In this article, we will be looking at 15 simple ways to improve your finances today!

Here are ways to improve your finances

1. Have A Close Look At Your Lifestyle

Can you really afford your lifestyle? It is sad to find out that there are people who cannot fund the life they currently live. You might ask how this is possible. For fear of missing out, people go into debt just to acquire luxury items and lifestyle.

Take, for instance, eating at restaurants can be expensive. Consistent eating at restaurants instead of cooking at home can be devastating on your finances.

There are various lifestyle habits that cost you more than needed. That is why it is important to have a vivid examination of your lifestyle. Do you buy things on impulse? That should be noted. Are you trying to impress your friends? Take care of that too.

The first step to improving your finances is to take a close look at your lifestyle. Do you prefer to buy pricey drinks and avoid unbranded products? It is imperative to examine your lifestyle deeply. Identify how your hobbies cost you more than they should. It will be helpful to record the precise number of beer bottles.

2. Check Your Credit

A credit report is a detailed breakdown of an individual’s credit history prepared by a credit bureau. A credit history is a record of a borrower’s responsible repayment of debts.

Your credit report helps you to track your spending and know your creditworthiness for a loan application. It is important to have accurate knowledge of your credit history to guide your spending.

With your credit report, you can make a priority list to know the urgent things to be paid for. By doing this, you develop the discipline to manage and improve your finances.

Credit reports are vital for loan and credit assessments. By knowing your current credit state, you have the chance to determine your financial value and pursue improvement.

3. Define Your Financial Goal

A goal is a good thing to have. Goals determine habits and systems. Set a financial goal. The goal you set will determine how you rearrange things to make your goal work.

Define your financial goal by stating how much you earn, how much you want to spend, and how much you want to save. If it is possible, state how much you want to earn.

By setting a new goal, you will be filled with motivation to improve your finances. Also, define your financial goal using a timeline; be it per week, per month, quarterly and yearly.

In essence, have short-term, mid-term, and long-term goals. A financial goal should reflect your investment goals, college funds, retirement funds, and insurances. Your financial goal should be clear and straight to the point. Keep it where you can see it and be reminded. State the time to clear off a part of your debts.

A goal reminds you, where the daily distractions compete for your attention, why you need this journey. You might want to be a millionaire by 40. You might want to save a good amount for your kids’ university education. A properly documented financial glory keeps you reminded and saves you from reckless spending. Be rigorous, yet optimistic when drawing your financial goal.

4. Make A Finanical Plan

You need a plan. A goal is unachievable without a plan. It is time after defining your goal to lay out a plan to make your goal a reality. Your plan is your step by step action needed to achieve your goal. A good financial plan should include details about cash flow, savings, debts, investments, insurances, and other elements of your financial life.

Take note of the standard of living in your city. If you can, make plans to find a new apartment to align with your goals. With these details, your strategies to achieve your goal will become clearer. A financial plan should ease your stress about money, support your basic needs and provide shelter for your long-term goals.

With a financial plan, you can make the best of your assets and ensure you meet your future needs. You can create a financial plan on your own or with the help of a professional. However you choose to create a financial plan, you need a plan.

When making a financial plan, lay your hands on as much information you can find. Learn about taxes, interest rates, cost of living. Let the ensuing facts and details guide your plan. Your plan matters every step of the way. Let it be a plan that can withstand the tests of time. Get a plan.

5. Create A Budget Now

How do you ensure that your expenditure is in line with your income? Simple, create a budget. A budget is an itemized summary of intended expenditure. Use your current income to prepare a budget.

A budget saves you the tragedy of impulse buying. People who pick things as they like off a supermarket shelf do not have a disciplined and rigid budget. Create your budget and stick to it.

A budget gives you clarity on what you need and what you do not need. Remember to give priority to pressing needs. Pressing needs include rent, food, light bill, credit debts, and other necessities.

Start with getting your financial papers and documents to track your expenses before the time. Get your receipts, bills, bank statements from previous months. Itemize your intended expenses for the month. With your net income, allocate to every item the amount as required.

Do not leave out things like entertainment, money to buy your friends gifts, and money to eat out. However, they should not top the list. Keep your budget as clear and accurate as possible. Write a list, it’s not a budget until you have written it down.

6. Cut Back On Your Monthly Expenses

Yes, there are things you can do without. Cut back on your monthly expenses. Make plans to have fun weekends at home without having to go out to make greater expenses.

You may want to cut some magazine subscriptions (sorry but yes). Cut out the unnecessary coffees. If you can walk to work, all the better. You can choose to cycle to work.

This is not only good for your finances but your physical health as well. Make your lunch to work. Put off the light bulbs when leaving the house, which cuts your light bill.

You may want to do a garage sale and sell off the things you do not need. You will save space and gain money. This is one important and easy way to positively improve your finances.

Here is a list of some things you can cut out of your monthly expenses that are not entirely important and you can completely live without. I personally saw a positive improvement in my finances by cutting these things out of my list.

7. Update Your Personal Finance Knowledge

Knowledge is power. Learning is good for the mind as physical exercise is good for the body. Financial literacy is a crucial element of improving one’s finances.

Update your personal finance knowledge. Financial literacy is necessary to make financially responsible choices that are needed for everyday life. Finance knowledge is important to your spending, saving, and investing.

With the right knowledge, you can make the right choice of an investment plan that aligns with your financial goal. After making your financial plan, consistently update your finance knowledge to make good changes to your plan.

Finance knowledge for an entrepreneur would be to understand supply and demand, and the value of money. Know how inflation hits and its effects. Good finance knowledge should prevent you from giving in always to the consumer’s instinct. It keeps you aligned with your goal and a desire to improve your income.

8. Work Towards Improving Your Income

Do not stay on one level of earnings. Seize opportunities to improve your income. You can leverage on free courses available online and MOOCs from top universities to improve your knowledge professionally and stay relevant in your field. Then push for a salary increase.

If you are self-employed, consider creating greater value for your customers. Money is the reward for value, so the more value you create, the more you can earn and scale up your business.

Explore genuine investment models and schemes for long-term income. The internet has made information decentralized, up to financial information that one would think was reserved for only those on Wall Street.

Sell your used items online. Might not be much, but it is honest work. If you have a car, you could register with Uber to drive people going in your direction while driving to work. Incase you are wondering about the best legal and possible ways to make money I have created a finanical guide on 200 easy ways on how to make more money today.

You could also drive back and earn some money on your way back from work. You can use your hobby or skill as a side hustle. You would enjoy being creative, relaxed, and earning all at the same time. Teach what you are really good at. Never forget to invest. Investment will secure you in the long term.

9. Master Your Money Mindset

What mindset do you have about money? Your money mindset drives the key decision you make in your finances. Your choices are a reflection of your mindset. Are you scared when you face a financial challenge or are you positive? A positive mindset works.

A negative mindset about money is what stands between you and seeking a way forward in your finances. A positive mindset makes the challenges easier to bear. It provides the motivation to go on as if everything is OK.

How do you master your mindset? Well, like every other mindset, watch your money thoughts. What comes to your mind when you receive a bill? Is it a necessity that you read as a burden? If it is a burden, you can discard it. If it is a necessity, you will take care of it. You will find a way.

To master the mindset, consciously identify and recognize your current state. Are you depressed about debts, accept that you are. However, don’t stop there. Now that you have identified your state, take responsibility. If you want to improve your finances, you must be responsible.

Quit blaming others. If you keep blaming others, you will lose the willpower to make corrections where you can. Forgive yourself. You may have made mistakes and wasted money. Forgive yourself. Give yourself a chance to turn things around. Then be grateful. Contentment is helpful to smart finances. Be grateful all the time.

Remember you are building a new mindset. You will be tempted to complain. You will complain but catch yourself in the act and remind yourself to be grateful. Write your vision and goals. Keep your goals, plans, and strategies where you can see them. By doing all these you will become the master of a positive money mindset.

10. Start Building An Emergency Fund

An emergency fund is money kept away that can be used in times of financial distress and crisis. This should be a part of your financial plan. Emergency funds provide financial security in cases of illness or to meet an immediate unplanned need.

Start by determining how much you want to save. Calculate, based on your net income a favorable percentage you can keep away for an emergency fund. Then, set a weekly, or monthly saving goal. It is preferable to move this saving automatically from your regular account to a saving account to avoid temptation.

You can use software or financial applications for this. Assess your savings over time and make adjustments when necessary. No amount of emergency funds is too much, so do not get complacent.

Most importantly, define in clear terms and separate from other incidents what you might term an emergency. Not everything is an emergency. Some things can wait, some cannot.

Breaking your emergency funds should feel like a painful necessity. In a good sense, your emergency funds should be a last point of call. If you can, save beyond your goal. Set a new saving goal and beat it again.

11. Create A Debt Reduction Plan

Tackling one’s debt requires time and effort. Debts are overwhelming. They induce worry at the thought and remembrance of it. But with good planning and strategy, you can reduce your debt and eventually become debt-free.

Start by avoiding more debt. You cannot work your way out of debt by getting into more debt. Take a break from using your credit cards. Switch to cash payment to remain conscious of your spending.

If possible, make a daily budget. Create a daily budget. Cross off anything you don’t need and don’t buy things you merely like.

12. Keep Track Of Every Penny That You Spend

So, every penny counts, including the penny for your thoughts. When you know how all your money is spent, you can decide how to make adjustments as needed. For the umpteenth time, pay in cash.

Yes, it seems difficult but I believe the stress involved with counting and laying down the cash keeps you conscious of what you are doing. Credit cards cushion the slight pain that comes with spending. Paying in cash ensures that you can feel like Jesus, that virtue has left you.

Next, create a log. It could be a physical notebook, a digital notepad, a spreadsheet, or a personal finance software/application. What matters is to create a log and use it dutifully. Write down every amount you get and the date it came in. Write down, for every single thing you pay for.

If done well, a good tracking will help you see money for what it is- a tool. This will improve your mindset. It gives greater awareness and you will become more confident at handling money. Write down every penny you spend, even if it was an impulse buy that you regret.

Do not leave anything off the list. Be careful with transactions that are easy to forget. If possible, get receipts for everything. You can, at the end of the day, week or month go through your log to spot the faults in your spending. By keeping track, you will have the full facts needed to improve your finances. Don’t forget to make that log.

13. Live Below Your Means

How? Simply put, living below your means is spending less than you earn. If you were to subtract your expenses in a month from your income that month, would you be left with a positive figure or a negative figure? If it is a positive figure then you are living below your means. If you are left with a negative, there is work to do.

The key to living below your means is styled in this question; “do I really need this?” Do you need it or like it? Do you need it or does your friend have it? If you cannot afford brand clothes and shoes, you can still get good shoes at cheap prices that won’t punch a hole in your finances.

Why continue paying for the gym membership when you can go on a run every morning? Wait, why pay for the gym if you won’t go at all? The idea is not to rob you of having a pleasant life. But there is no pleasant life when debts are clutching at your neck.

Reduce your spending. Your favorite drink costs more, yes it is time to change it. Live below your means while seeking to improve your income. Before you make that payment, ask yourself if it is a need and if you could improvise. Improvise where you can.

Cook your meals at home and keep them in the freezer. Take your lunch to work. Renegotiate your interest rates. Downsize your home. It takes sacrifice, discipline and a good mind to do all these. The benefits however are worth it. You would experience less anxiety as you take control of your spending. It pays off in the long-term and you will be glad that you lived well below your means.

14. Beware Of Expensive Habits

Remember when you had to take a close look at your lifestyle? This should come in handy. Expensive habits like drinking, wasting groceries, shopping for pleasure, can affect your finances. We have all made poor choices in our finances and picked up habits that cost us more than we think. But if you must improve your finances, you must cut some of these expensive habits.

Cut out that hobby. I know you like to try out every new hobby your friend tells you about. But hobbies cost money to enjoy them. Use your friend’s golf clubs instead of getting a new one.

You can decide to quit golf and play chess. Quit shopping because you loved your friend’s new shoes. You don’t need those shoes. Comparing yourself to other people is an expensive habit that costs you in finances and mindset.

Step by step, reduce the number of bottles of your favorite drink. You can do without it. Cut that habit. You can host friends and tell everyone to bring their cookies, cakes, and pizza. Enjoy the pleasures of your home without spending much outside.

15. Embark On A Spending Break

Create avenues to avoid spending at all. You should have things set up so well that for at least a day, you shouldn’t have to spend any money at all. That is a spending break.

With a good budget, cook your meals on a weekend that could last you a whole week and store them in a freezer. Fill bottles of water and place them in a refrigerator. Warm your food when hungry and at home. Avoid the temptation to order pizza.

When you are not going to work, maybe on a weekend, eat your home-cooked meal, drink your water and watch television. Avoid the craving to go out unless it is too important. Enjoy DIY therapy. Take a cold shower to be relaxed.

I want you to know that having your finance balanced is a very important and vital part of your self-growth and self-development. A person who isn’t financially balanced or progressing financially in life won’t be able to make positive progress.

So take your time to implement these tips. You don’t have to do everything immediately slow and steady but the most important thing is that you are taking steps to positively improve your finances no matter how small.

Question of the day - What's one financial goal you have?

Money & Finances

What's one financial goal you have?

Daily archives

Current Survey

Top 5 Contributors (Apr)

22448 pts

20209 pts

14197 pts

12060 pts

11932 pts